What to Expect in Your First Year Investing in Alternatives

.jpeg)

Steve Dean is the Chief Investment Officer at Compound. He has 30+ years of experience in markets and investments, and leads our investment team, developing our public and private model portfolios. He previously worked in the economic research department of the Federal Reserve.

Alternatives aren’t necessarily complicated, but they’re nuanced. They look and act differently than standard public market investments.

The capital doesn't deploy on day one. The tax documents arrive late, in a different format. And for the first year or two, your portfolio can look like it's not growing at all. These differences — across fund structures, capital call schedules, tax reporting timelines, and liquidity trade-offs — make people apprehensive about alts, and many end up under-allocating.

The investors who get the most out of alternatives aren't just good at picking funds. They understand how alts behave before they invest, which means the early mechanics don't catch them off guard. The J-curve, capital calls, and K-1 tax reporting are predictable, so they’re prepared for them.

When you set yourself up to handle these factors in advance, you’ll be prepared for the early days of investing, and poised to reap potential benefits later. When you’ve spent months evaluating alternatives, it’s important to bring that level of care to your post-investment planning, too.

Key takeaways:

• Most alt investments require patience. Early performance will look flat or negative. This is by design, not a red flag, and investors who understand this are poised to benefit in the long run.

• Your entry point and vintage diversification matter. High valuations during your entry into alternatives can compress your returns; investing in a new fund each year hedges against this.

• Capital calls demand liquidity planning. Setting up a dedicated liquid account before year one is a concrete, practical step that prevents overcommitting funds, which is a common mistake.

Why Alternatives Belong in a Diversified Portfolio

Your public portfolio might be returning well, and it’s much easier to understand than private equity. You might be asking why bother with alts when I’m already doing well?

Private equity has the potential to generate better returns than public equity. Similarly, private credit has the potential to offer a higher yield than traditional bonds. Real assets tend to move differently from both.

Alts usually offer less liquidity and less correlation to the markets you already have exposure to, and in exchange, you get a return profile and layer of portfolio resilience that public markets alone may not offer.

It’s a more complicated and nuanced investment, which comes with the territory of investing in things that aren't publicly traded. That's also why they return differently.

And they require some more patience. For private equity and VC specifically, we often remind clients that the first few years won’t look like much, and that’s expected. During this time, your portfolio performance might look flat, even slightly negative.

Once you pass that threshold, you may start to see distributions from your earliest fund. That’s often when you can see returns and the long-term benefit of waiting. It’s at this time that you can evaluate whether they’re working for you.

On the other hand, private credit behaves differently: It typically pays monthly or quarterly distributions rather than asking you to wait. Those distributions are taxed as ordinary income, so if you're still in accumulation mode, the tax drag can outweigh the yield.

Private equity and private credit are just two kinds of alternatives available to you. I break down more on alts and how they work for different investors in this Manual.

Once you decide to move forward with alternatives, two factors will shape your experience more than anything else:

Your entry point matters. Private equity returns vary by vintage — the year you invest affects what your manager pays for companies, and that shapes your ultimate return. If you diversify vintages, then a rolling program can help with the variance in entry points.

For example: Investors who are buying into PE or venture-backed AI companies now — when valuations are elevated — might see softer returns than a prior vintage that invested when the same companies were priced lower. Vintage diversification can help solve for pricing variations across years. Some years will inevitably be better entry points than others, and a rolling program smooths that variance over time.

The timeline requires genuine patience. The investors who see the best results are generally the ones who stay the course through initial roadblocks, before returns are visible and before the program feels like it's working. That's when it matters most.

Before committing to alternatives, knowing the friction points upfront changes how you prepare. And one of your first decisions — a drawdown or an evergreen fund — determines which friction points you'll actually face.

Drawdown or Evergreen Fund: Which Is Right For You?

The first decision you make is which type of fund to invest in — drawdown or evergreen fund — and it’s the most consequential. Your choice determines what sort of relationship you’re going to have with your money moving forward.

Are you along for the ride, or do you need to have more frequent views of the value of your investments and the possibility of more regular access to your money?

In a drawdown fund (closed-end) you commit capital, the manager calls it in stages as opportunities arise, and you see results ~7-10 years later when companies are sold, go public, or get acquired. You’re basically along for the ride — in fact, you’re locked into it. Illiquidity is a risk, of course. With drawdown funds, part of what you’re being paid for is your willingness to carry that risk.

An evergreen fund (open-ended) might look a bit more familiar: It offers more frequent valuations and periodic (often quarterly) liquidity windows, which means you may be able to access funds more easily. It is important to understand that these liquidity windows have restrictions. Filling all of an investor's redemption request is not guaranteed as total withdrawals will typically be limited to 5% of the funds total value. If the fund redemption requests are more than this 5%, investors will get a prorated withdrawal amount. These limits are meant to protect investors in the funds from forced selling of sometimes illiquid underlying assets. Still, these funds are more flexible, and usually tout lower required minimum investments.

Deciding which fund to invest in determines your liquidity profile, your vintage diversification timeline, and the operational complexity of managing your program.

Neither structure is necessarily better than the other — it just depends on the investor’s personal situation.

Three factors that determine which structure is right for you:

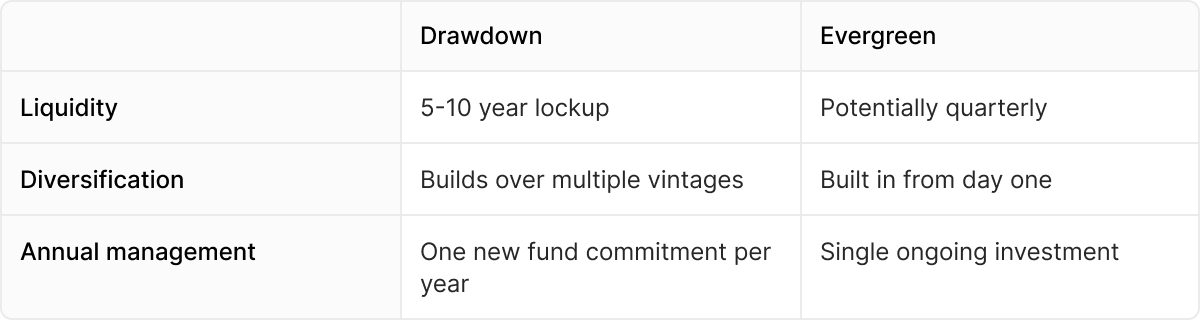

#1: Liquidity profile. How reliably can you commit capital for 5–10 years without needing it back? Many investors overestimate how much liquidity they need, so they should discuss that amount with an advisor.

Which fund fits? Drawdown funds could work well for investors who can genuinely commit to a longer time horizon; however, they do need to make a new fund commitment every year. Evergreen or interval funds, with their potential for quarterly liquidity, may fit investors with less predictable liquidity needs, but there’s a chance of lower return as those funds take on less liquidity risk.

#2: Vintage diversification. Investors who have spent years investing in alts have naturally stacked multiple fund vintages. But a first-time investor starts with only one vintage, which means they won't become diversified for years.

Which fund fits? Evergreen funds, which already hold a portfolio of investments across multiple entry points, can solve for this concern immediately — but they may need to hold a portion in more liquid assets to meet redemptions, which can create some drag on returns. Drawdown funds are single vintage, but investors can avoid the single-entry point issue by building a rolling program across multiple vintages; however, that requires ongoing account management.

#3: Annual management and operational simplicity. In a typical drawdown program, investors often commit to a new fund roughly every year over a five year period to build vintage diversification across their portfolio. That means five separate capital call schedules to track, five K-1 timelines, and five entry-point decisions.

Which fund fits? An evergreen fund gives you alts exposure but removes the sequencing work and annual program management. The trade-off is that you're buying into a more mature portfolio instead of getting in at the earliest stage. Plus, the operational simplicity might come with less return potential, depending on the opportunity set. A drawdown fund requires annual program management, and is more complicated, but the returns can be higher if the fund picks a more concentrated and vintage specific.

If you're entering a drawdown fund, there are three friction points worth preparing for.

Friction Point #1 — The J-Curve: Why Early Returns Look Flat

One friction point drawdown fund investors face is the J-curve.

Think of the J-curve like an optical illusion: your money’s committed, but it looks like the value of the investment is actually declining out of the gate. That’s the initial downward shape of the “J” and the pattern could continue for months, or even years.

But know that the J-curve is a natural part of the process: It’s what happens before invested capital starts generating returns. The fund is spending the clients investment dollars finding and making deals. But, those investments haven’t begun to pay off. It can just feel a bit underwhelming in that early period. Investors who stay the course know the J-curve is often temporary, with an upward trajectory in fund value to come, and not a signal to exit.

Over the years that follow, you can reduce the psychological impact of the J-curve with vintage diversification: investing in a new fund every year. That rolling investment will keep you from feeling inactive or that the investment is under performing.

Friction Point #2 — Capital Calls (The Money You Feel Like You've Already Spent)

Capital calls are a close cousin to the J-curve friction, and they can raise negative sentiment for first-time investors. The capital call structure occurs in private equity and venture capital drawdown funds.

How capital calls work

In a drawdown fund, you don't send your full committed amount upfront: The fund draws it down in installments as it deploys your investment into deals — sometimes on a published schedule, sometimes episodically. For example, a fund could require 20% on day one and then 20% for each of the next 4 quarters, with fully called capital after that full year. The predicability of that schedule varies by fund, which is why it's one of the first things to ask about.

You need to be able to release those funds at the time of the capital call. A common approach is to set up an account that holds the committed capital before the first call arrives. Holding those funds in a money market or another liquid vehicle allows you get some return on that capital. When investors commit to an investment amount and put those funds at risk in the market, a downturn could leave them short when the capital call arrives, but they're still on the hook for the full amount.

Friction Point #3 — K-1s and Tax Reporting (Expecting the Filing Extension)

Most drawdown fund alternative investments generate K-1 tax forms that typically arrive later in the year — sometimes not until September. This friction point hits the investors who are used to filing by April 15, whether they do their taxes themselves or work with a preparer.

Investors who have complex financial pictures that include equity compensation, existing partnership interests, real estate investments, or other K-1-generating assets likely already file an extension. For those who are new to this, it can be a psychological barrier: They like their taxes buttoned up early, but they will now need to extend the deadline.

If this is a first for you, simply knowing that the K-1 is coming and discussing with your advisor can help you stay confident that you will still meet the tax deadlines.

A few things to keep in mind with K-1s:

- Some funds help solve for the K-1 timing headache. More and more alt providers are offering vehicles that generate 1099s instead of K-1s. These are primarily evergreen or interval funds

- Some K-1s are more complex than others. If a fund holds international investments, it could generate a K-3 as well, adding another layer of reporting complexity. This is worth asking about before you invest. Some funds may also generate Unrelated Business Taxable Income (UBTI) which could require additional tax form requirements for certain account types, like IRAs.

- Tax coordination matters. When you have a complicated equity and alts picture, it’s beneficial for your advisor to speak directly with your CPA. At Compound, our advisors coordinate with your CPA and our internal tax team so the K-1 timing and extension process is handled, and isn’t something you’re tracking down yourself.

If you’re expecting a K-1, it’s recommended you get the tax conversation on the calendar before your first investment closes. You should make sure your preparer has dealt with K-1s, understands the extension timeline, and knows whether the fund might generate any additional tax complications..

That way, there are no surprises when tax season rolls around, or when the K-1 form arrives in September.

Summary: Questions to Ask Your Advisor Before Year One

When you’re investing in your first fund, have these four questions answered.

- Is this a drawdown fund or an evergreen/interval fund? The J-curve, liquidity features, and diversification profile all differ depending on the fund’s structure.

- What is the capital call schedule, and how reliable is it? Some funds publish a schedule; some only give estimates. Knowing which you're in changes how you structure your capital account.

- What liquidity do I really need over the next 5–10 years? Some investors overestimate how much liquidity they need. Make sure you have an explicit conversation with your advisor about what makes sense according to your financial picture.

- Does this fund generate K-1s or 1099s? If K-1s, make sure your tax preparer has dealt with them before and understands extension timelines.

FAQs

How long should I expect to wait before seeing returns on my alternatives investment?

Plan for a minimum of 5–7 years. In the early years, your portfolio may look flat or even slightly negative, but that’s normal. Once you pass that threshold, you'll start seeing distributions and can really evaluate performance.

What's the difference between a drawdown fund and an evergreen fund, and which is right for me?

A drawdown (closed-end) fund draws capital in installments over time; it might be better for investors who can reliably commit money for 5–10 years. An evergreen (open-end) fund offers the potential for more frequent liquidity and built-in vintage diversification, meaning it’s often preferred by investors with less predictable cash needs — though it may have slightly lower return potential.

Will investing in alternatives complicate my taxes?

Most likely. Many alternatives generate K-1 tax forms, which often arrive well past April 15th meaning you'll need to file a tax extension. Before your first investment closes, make sure your CPA has experience handling K-1s and understands the extended timeline.