Golden Handcuffs: How to Decide Whether Your Equity Is Worth Staying For

Tara Shulman is a Principal Wealth Advisor at Compound. She has extensive experience guiding clients at companies such as Figma, Anthropic, and Coinbase through IPOs, tender offers, and other company liquidity events.

Are you staying for the job, or staying for the vest?

If it’s the latter, you’re not alone. That’s the golden handcuffs and they look different depending on where you work.

At a private company, you could be holding options that haven't vested yet, so you feel tied to an exit event that you hope will happen someday. At a public company, your RSUs vest on a regular schedule, so it might feel like an extra bonus. That routine changes your income budgeting, and that can be hard to walk away from because that money has become a significant part of your lifestyle.

Equity can often act like an invisible tether. Not because people are consciously choosing to stay for it, but because the vesting schedule or the RSU quietly starts making the decision for them. Those golden handcuffs keep people in roles they've outgrown, and at companies they'd leave tomorrow if it weren't for what's still vesting.

Plus, the golden handcuffs can feel tighter the longer you stay. Two years into a four-year vest, you have a clearer picture of the potential upside — even if it's still on paper. And each new grant extends that timeline further.

Many feel they can't fully model their way to an answer when they have an equity package. Math alone can’t always answer the question: Is my equity worth staying for?

That question tends to crystallize at a specific moment — a cliff approaching, a milestone vesting, a new offer landing — and suddenly needs an answer.

The answer rarely lives in the equity alone. Instead, it lives in the full picture of your finances and what the money actually does for your life.

Key takeaways:

• Start with life consequences, not dollars. Anchor your equity decision based on what the money actually does for your retirement timing, housing, and lifestyle. That reframes "is $8M a lot?" into "does staying 18 more months meaningfully change my future?"

• Refresh grants and lifestyle creep are the hidden forces keeping you stuck. Overlapping vesting schedules keep moving the finish line, while RSU vests absorbed into monthly spending create a cash flow dependency that makes leaving feel financially impossible, even when it's the right move.

• Unvested equity is a negotiating asset, not just an anchor. Know the value of what you're leaving behind, and use it as the floor for any new offer. The structure of the new package matters as much as the big number.

3 Steps to Figure Out What Your Equity Is Worth — and What to Do With It

The math alone won't give you a clear answer. Your equity decision sits at the intersection of financial variables like vesting timelines, tax treatment, opportunity cost, and concentration risk. Then there are the harder-to-model ones, like career satisfaction, lifestyle, and what you actually want the money to do for your life. All of these factors matter and should play a role in your equity strategy.

Many clients come in having already run the numbers themselves — in a spreadsheet, or with an AI model. The issue usually isn't that the math is wrong. It's that it's missing the wider set of variables: opportunity cost, lifestyle consequences, the psychological cost of staying. That's the gap an advisor fills.

It’s also important to consider the factors outside of your control. Stock prices, exit timelines, and macro conditions are genuinely unpredictable. When we help clients get clarity around their equity decisions, the goal isn't to find the one right answer. We model various scenarios to help them understand what’s possible under a variety of circumstances.

It's typically beneficial to understand these factors well before your next liquidity event. Once an IPO is announced or a tender offer window opens, the timeline compresses fast. The decisions you make in those first weeks are harder to course-correct later.

At a private company, you're working with hypotheticals — an exit that may or may not happen, on a timeline no one can predict, at a valuation that hasn’t been market-tested.

At a public company, where the stock price is visible, your decision still involves variables that don't show up in a single share price.

Your decisions interact with your retirement timeline, your tax situation, your cash flow, and every other variable that shapes what the money actually means for your life. Below are the steps we walk through with our clients.

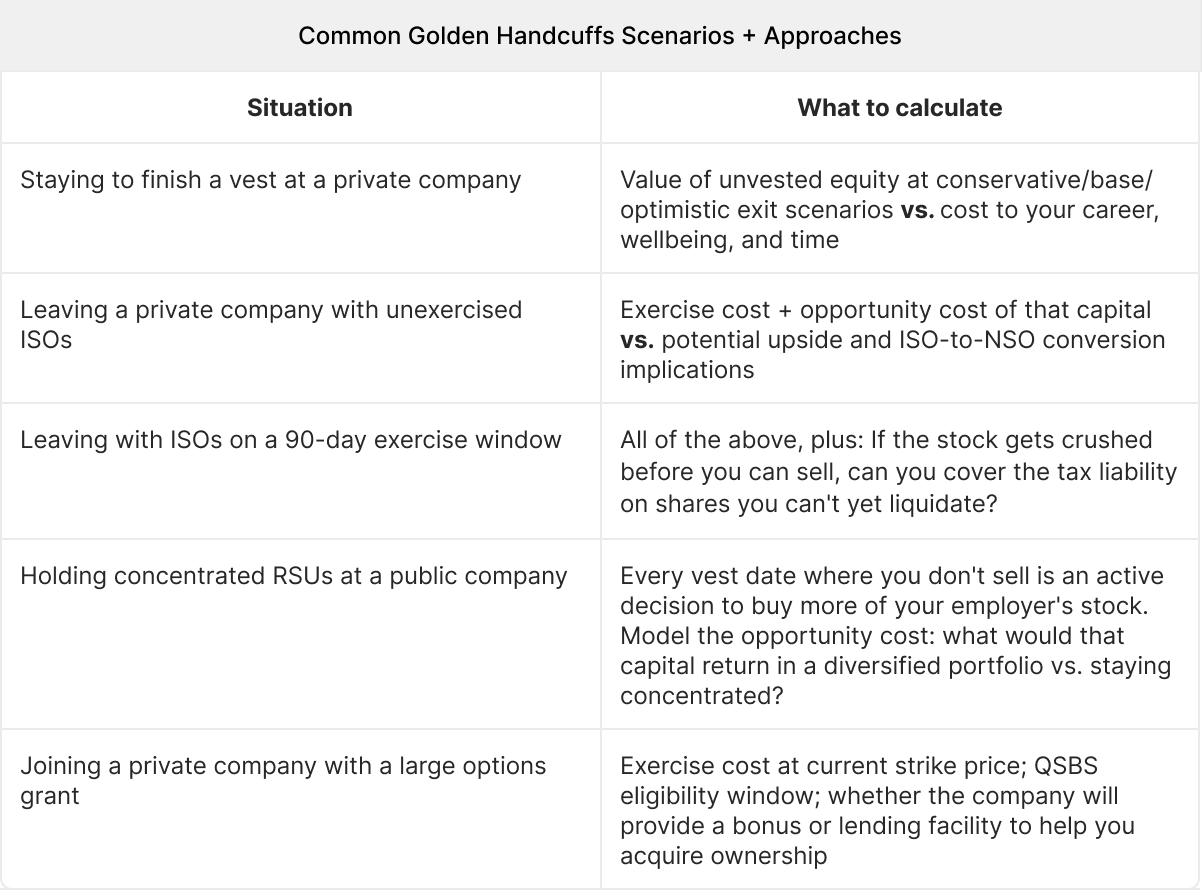

Step 1: Calculate the cost of staying vs. leaving the company

Many clients want to start with the equity decision: modeling scenarios at different valuations, and calculating the tax impact. Before we do the math, we ask, "Are you happy where you are?"

That answer changes everything. $1, 5, or 10M looks different if it lets you retire five years early than if it barely moves the needle for your life goals. Knowing what you're actually solving for is what makes the modeling meaningful because it reframes the possibilities in the context of your life.

The dollar amount is never the whole story. A stock that drops in value could still be enough to change your retirement timeline. One that doubles might be irrelevant against the wealth you've already built. The real question is whether that capital would do more work somewhere else. Your equity is an investment decision like any other, and it should be evaluated the same way.

What does staying cost you, in terms of opportunity, time, and lifestyle?

What does leaving cost you, in terms of unvested equity, exercise costs, and tax implications?

Some questions to ask as you evaluate:

- Can you pull your retirement forward by five years if this comes through?

- Can you afford to stay in your house/neighborhood long-term, or do you need to look elsewhere for more affordable housing?

- Do you want to fully retire, or would you be open to consulting?

These questions reframe any dollars-first thinking by changing the unit of measure: As opposed to saying “$8M is a lot of money,” you’re thinking through whether staying another 18 months to get that $8M affects your life in a way that an earlier exit doesn't.

Once you’ve thought about your lifestyle, you can run the numbers. In Compound’s equity modeling tool, we model unvested equity at different valuation scenarios, and run those outcomes through a Monte Carlo simulation against a full lifetime planning horizon to see the success probability.

But that’s not going to give you one clear answer either. It just helps you think about the bigger question: How does this equity fit into everything else?

Factor in opportunity cost as well:

- If you spend a million dollars exercising ISO options, that million dollars isn't growing in the market.

- Every RSU vesting date that you don't sell, you’re making an active investment decision. You're not passively accumulating shares — you're choosing to buy more of your employer's stock instead of putting that money somewhere else.

Whether you decide to stay, exercise, hold, or leave, there's a cost on both sides of the ledger.

If you work for a private company, liquidity isn't defined, and the timeline isn’t either. When you model, you need to create a number of hypothetical exit scenarios at different valuations and dilution levels. Anchoring in life consequences is especially important — while the dollar amount is speculative, you can still evaluate what different amounts would mean for your retirement, your housing, and your future.

If you work for a public company, the valuation is visible and the vesting path is defined, which makes modeling more concrete. What’s most important is to remember opportunity cost: holding a lot of employer stock is still a concentrated bet, and every vest date where you don't sell is a reinvestment decision.

Step 2: Recognize what lifestyle creep and refresh grants are costing you

The factors that make leaving difficult aren't always visible in the math.

For employees with options at a private company, it often comes up in their refresh grants. Each new grant adds new vesting timelines. The "what could be" narrative is compelling precisely because it's unresolved. Your time horizon is undefined, your exit is uncertain, and it’s easy to let that drive your decisions.

Pressure-test the narrative using financial modeling with your advisor. They’ll help you understand how each scenario could change the outcome for your long-term goals.

For employees with RSUs at a public company, it often comes up as lifestyle creep. Vests become part of their monthly cash flow and leaving means taking a pay cut. Both make the decision harder than it needs to be.

Your advisor can model what would happen to your cash flow when those vests stop. Although it may lead to some lifestyle changes, the impact tends to be more reasonable than clients initially believe.

What "sweating it out" can actually return

The math doesn't always justify the wait. Consider an employee who sold shares at a tender offer and spent years convinced they'd left enormous upside on the table. When the next tender offer came around five years later, the increase roughly matched what that cash would have returned in a diversified index fund.

They sweated out the decision for market-rate returns. When evaluating private company equity, build in a premium for illiquidity and the psychological cost of staying. If the projected return doesn't clear that bar meaningfully, the math changes.

If what’s keeping you at your company is lifestyle creep, ask yourself: Can I temporarily take on illiquidity to secure a potentially high-growth equity grant, and for how long?

If it's a refresh grant, ask: does staying through this next vest meaningfully change my financial picture?

Step 3: Negotiate a package that accounts for what you're leaving behind

Before you accept any offer, do calculate what you're leaving behind. That number is a significant lever, and a hiring company that wants you should account for it.

It’s often OK to make that ask explicit when negotiating a new offer. For private company employees, if the remaining equity vests on schedule and sells at a reasonable stock price, what does that yield? That number becomes your baseline, and the new package needs to clear it, and ideally exceed it. For public company employees, your unvested RSUs have a known dollar value. That number is your floor.

This is also where working with your advisor early makes a real difference. Before you're in the room negotiating, they can help you model what you're leaving behind, identify which terms are worth pushing on, and make sure the structure of the new package actually works in your favor.

What's actually on the table during a negotiation

The standard grant a new employer offers is just the starting point. You can also make requests regarding:

Equity buyout or sign-on bonus to cover what you're leaving

If you're walking away from unvested equity, you can ask the hiring company to compensate you for it. This might look like a cash sign-on bonus or an accelerated grant structure. Frame it plainly: "I have $X in equity that vests over the next 18 months. To make this transition work financially, I need the offer to reflect that.”

Accelerated vesting

You may be able to raise the idea of accelerated vesting — where shares vest faster than the standard four-year schedule, or potentially all at once. Even partial acceleration (say, a one-year cliff waived) could meaningfully change your early equity exposure. You typically don't see accelerated vesting unless it's a leadership team member or a key employee.

Extended exercise windows

If you're leaving a private company, you often have 90 days to decide whether to exercise your options or forfeit them. That window can be prohibitively short, especially if you have a long tenure or a large grant. It's worth asking a hiring team upon joining if your post-termination exercise window can be extended to two years, five years, or the full term of the option. That’s something to negotiate before you join the company, and it can’t be changed when you leave.

Exercise cost support — bonus or lending facility

At early-stage companies, the strike price on a large options grant can make exercising unaffordable. Ask the hiring company if their offer can include a bonus structure or internal lending facility to help fund the exercise. This is especially important for QSBS benefits, because accessing those tax advantages requires holding the stock, which means you have to exercise first.

Early exercise rights

Early exercising lets you buy shares at the current strike price, which can minimize out-of-pocket cost if the valuation is still relatively low. It also starts the QSBS clock earlier, giving you a longer runway toward tax-free treatment on gains.

QSBS and early-stage private companies

At early-stage private companies, the negotiation questions become more specific. The negotiation shifts from compensation to ownership. These are the questions worth asking:

- What percentage of the cap table is being offered on a fully diluted basis?

- What does that look like at different exit valuations and dilution scenarios?

- How will I pay for it?

At high strike prices, the exercise cost alone can be prohibitive. In situations like that, it's worth asking the hiring company about a bonus structure or lending facility to help fund an exercise — especially when QSBS benefits are on the table, which require you to hold the stock to access it.

Discuss early exercise, too: It might be able to minimize the out-of-pocket cost at current valuation and start the QSBS clock.

If you work for a private company, look into cap table percentage, dilution modeling at different exit scenarios, and whether the company will support ownership acquisition. Treat exercise cost as a negotiation variable.

If you work for a public company, RSU grants are usually quoted as a dollar amount that converts to shares, so the comparison across offers is more direct. Know the dollar value of what you're leaving behind, and use it.

Equity Isn't Passive. Your Decision Shouldn't Be Either.

Free yourself from the pressure of thinking there’s one correct decision.

No matter what you do, equity values, exit timelines, and macro conditions are genuinely unpredictable.

If you work for a private company, make sure there's a real model behind your decision and a clear sense of what you’re working toward. If you leave, know what you're giving up and why the trade is worth it.

If you work for a public company, the main risk is inertia. Years can pass while refresh grants and lifestyle creep make it difficult to see that you’re actively making investment decisions back into your company. Your decisions should be based on your goals, not your vesting schedule.

As you start considering your equity compensation and what the cost of leaving looks like, you can see your equity against the rest of your portfolio, and our advisors have planning tools to model scenarios for your personal situation. That’s how you can start developing the full-picture analysis you need to break out of those handcuffs.

The biggest question is whether you’re happy. Your advisor can help you build in a premium both for illiquidity and the psychological cost of staying. If the projected return doesn't clear that bar meaningfully, the math changes.

FAQs

How do I know if my equity is actually worth staying for?

Start by calculating your "walk-away number" — what the equity would concretely mean for your life (retirement timing, housing, financial freedom). Then model the scenarios: for private companies, run conservative, base, and optimistic exit valuations; for public companies, factor in opportunity cost and concentration risk. If the projected return doesn't meaningfully clear the bar after accounting for illiquidity and the psychological cost of staying, the math may not support it.

What happens to my unvested equity when I leave a company?

It depends on your equity type and timing. If you have ISOs, you typically have a 90-day window to exercise after leaving — which means you need to weigh exercise cost, potential tax liability, and the risk that the stock drops before you can sell. RSUs at public companies are generally forfeited if unvested. In either case, the unvested amount can be a negotiating asset with a hiring team, who may offer a grant to offset what you're leaving behind.

How do I compare an equity offer from a new company against what I'm giving up?

Look beyond the numbers. Key variables include whether the new grant is public vs. private, RSUs vs. options, and how the vesting schedule is shaped year by year. At early-stage companies, shift your thinking from dollar value to cap table ownership percentage, and model that across different exit and dilution scenarios.